1099 vs W-2, Explained

"1099" and "W-2" are just IRS form names, but they describe two very different working relationships with very different economics. If you are weighing a contract role against a salaried job, or deciding how to structure your own work, understanding the gap between them is worth real money. Here is what actually separates the two.

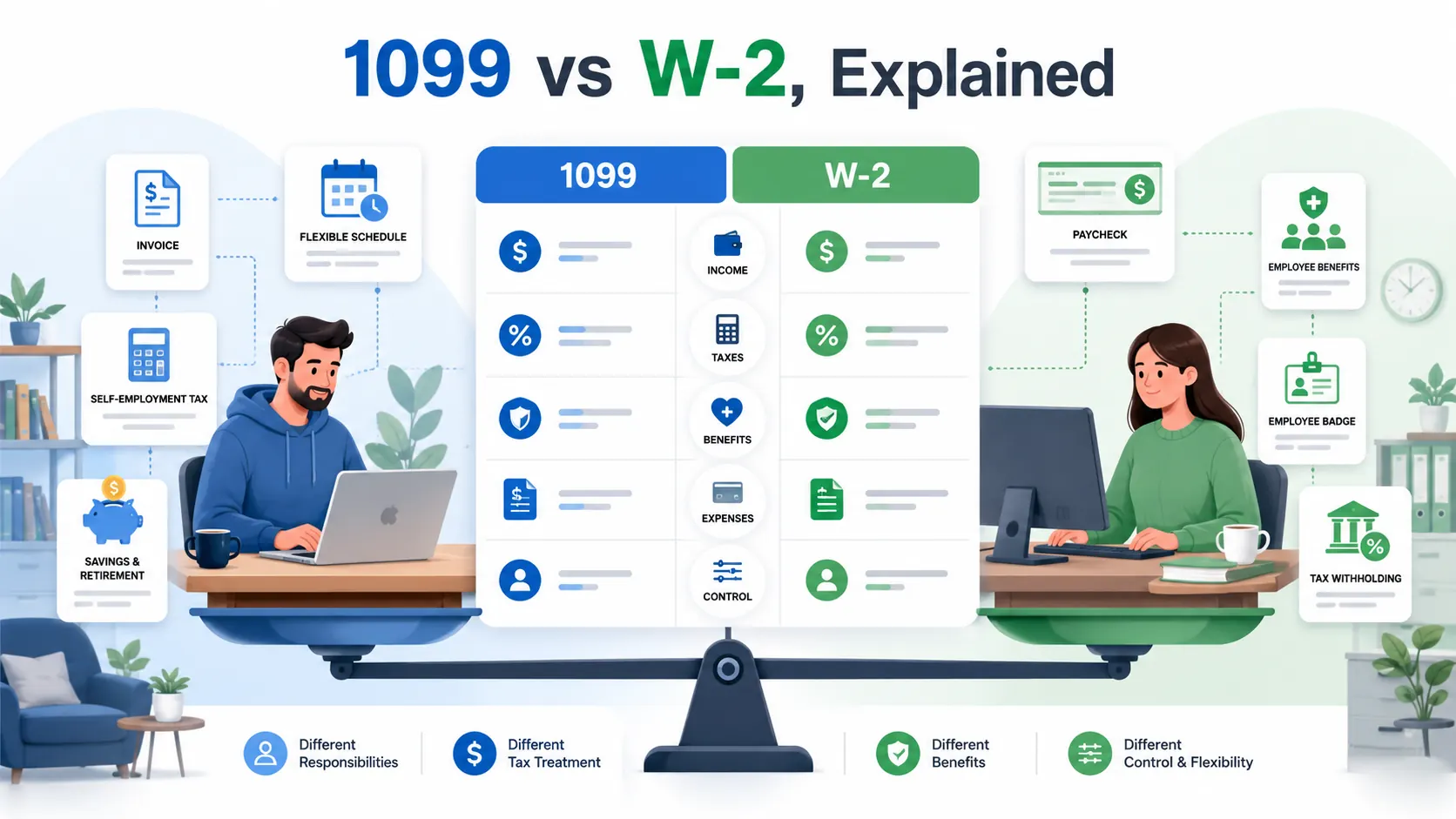

The legal and tax difference

A W-2 employee works for a company that directs how and when the work gets done. The employer withholds federal and state income tax from each paycheck, pays half of the employee's Social Security and Medicare taxes, and reports it all on a Form W-2 at year-end. A 1099 contractor is an independent business providing services to a client. The client pays the full agreed amount with nothing withheld and reports it on a Form 1099-NEC. The contractor is responsible for their own taxes.

Classification is not a free choice. The IRS weighs behavioral control (does the company control how you do the work), financial control (who provides tools, who can profit or lose), and the nature of the relationship. Companies sometimes misclassify employees as contractors to avoid payroll taxes and benefits, which is illegal; the facts of the relationship, not the label, determine the correct status.

The hidden employer burden

The most expensive difference is also the least visible. Social Security and Medicare together cost 15.3% of earnings. A W-2 employee only sees 7.65% come out of their paycheck because the employer quietly pays the other 7.65%. A 1099 contractor pays both halves - the full 15.3% self-employment tax (on 92.35% of net profit). That alone is a meaningful pay cut unless the contract rate accounts for it.

On top of payroll taxes, employers carry other costs you never see on your offer letter: unemployment insurance, workers' compensation, and the overhead of payroll itself. When you go independent, those costs either disappear or land on you.

The benefits gap

Beyond taxes, a salary usually comes bundled with benefits that have real dollar value:

- Health insurance, often heavily subsidized by the employer. A contractor buys their own, frequently at full price.

- Retirement matching, such as a 401(k) match that is effectively free money. A contractor funds 100% of their own retirement, though plans like a SEP-IRA or Solo 401(k) allow large contributions.

- Paid time off, holidays, and sick leave. For a contractor, time not worked is time not paid.

- Other perks: life and disability insurance, training budgets, equipment, and a steady paycheck regardless of workload.

Add it up and these benefits can be worth 20% to 40% of a salary on top of the headline number - value a contractor must recreate out of their own rate.

Pros and cons of each

Neither is universally better; they suit different priorities.

- W-2 strengths: stable income, benefits, half your payroll tax paid for you, simpler taxes, and protections like unemployment insurance.

- W-2 trade-offs: less control over your schedule and clients, a single income source, and a hard income ceiling.

- 1099 strengths: higher potential earnings, control over your rate, clients, and hours, the ability to deduct business expenses, and access to the 20% QBI deduction.

- 1099 trade-offs: no benefits, the full self-employment tax, income that rises and falls, no paid time off, and the administrative load of running a business.

The true-wage idea

Because the two are so different, comparing a contract rate to a salary at face value is misleading. The honest way is to convert both to a true, after-tax value. Take the salary and add the dollar value of its benefits to get the W-2's total economic worth. Then take the contract income, subtract self-employment tax and the cost of buying your own benefits, and spread it across your actual billable hours. Only then are you comparing like with like.

When you run that math, a contract rate typically needs to be 25% to 50% higher than the equivalent salaried hourly wage just to break even - and more if you want to come out ahead. Rather than do this by hand, drop both offers into our 1099 vs W-2 calculator, which computes the after-tax value of each side and tells you the exact break-even hourly rate you would need to charge as a contractor.

So which should you choose?

If you value stability, benefits, and simplicity, a W-2 role is hard to beat. If you value autonomy, higher earning potential, and the tax advantages of running a business - and you can handle variable income - 1099 work can pay off handsomely, provided you price it correctly. Whichever path you are on, the key is to compare on true value, not the sticker number.

Compare an offer the honest way

See the true, after-tax value of a contract rate versus a salary, plus the break-even hourly rate you would need to charge.

Open the 1099 vs W-2 calculator